New Optimization Method: HERC

We've added a new portfolio optimization model to your toolkit: Hierarchical Equal Risk Contribution (HERC). This advanced optimization model splits portfolio assets into clusters that share similar price movement patterns, like growth stocks, crypto, bonds, etc. Then those clusters are rebalanced so that each contributes equally to overall portfolio risk, preventing any single asset group from dominating your portfolio's risk exposure.

HERC is similar to HRP but tends to produce less conservative allocations by balancing risk contribution rather than simply giving less weight to riskier groups. Unlike traditional methods like Mean-Variance Optimization, HERC tends to outperform out-of-sample, meaning it performs better on future data it hasn't seen before. This makes it more robust for real-world investing.

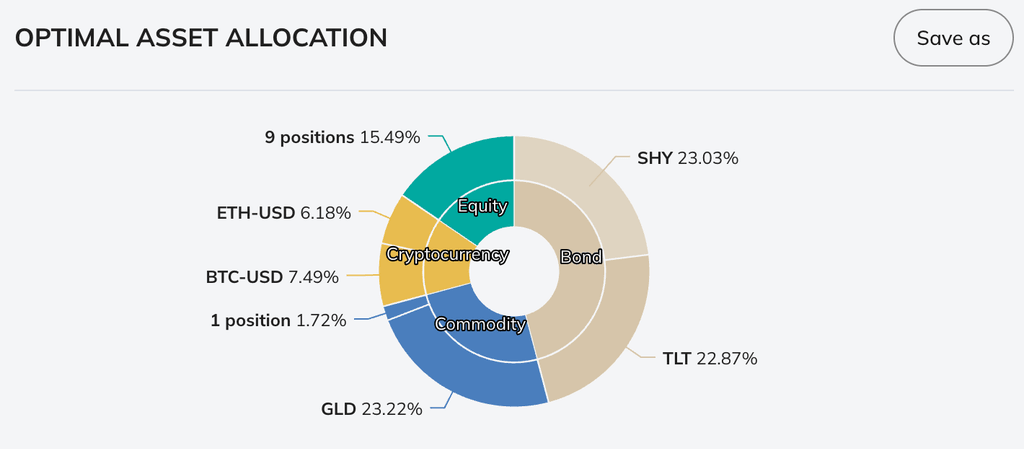

HERC automatically identifies natural asset groupings and balances risk across them. In this example portfolio, the optimizer distributed holdings across defensive bonds, growth equities, and cryptocurrencies for balanced diversification.

The optimizer grouped this portfolio into 3 distinct clusters based on correlation patterns: bonds and gold (safe haven), stocks, and crypto. Each cluster contributes equally to total portfolio risk.

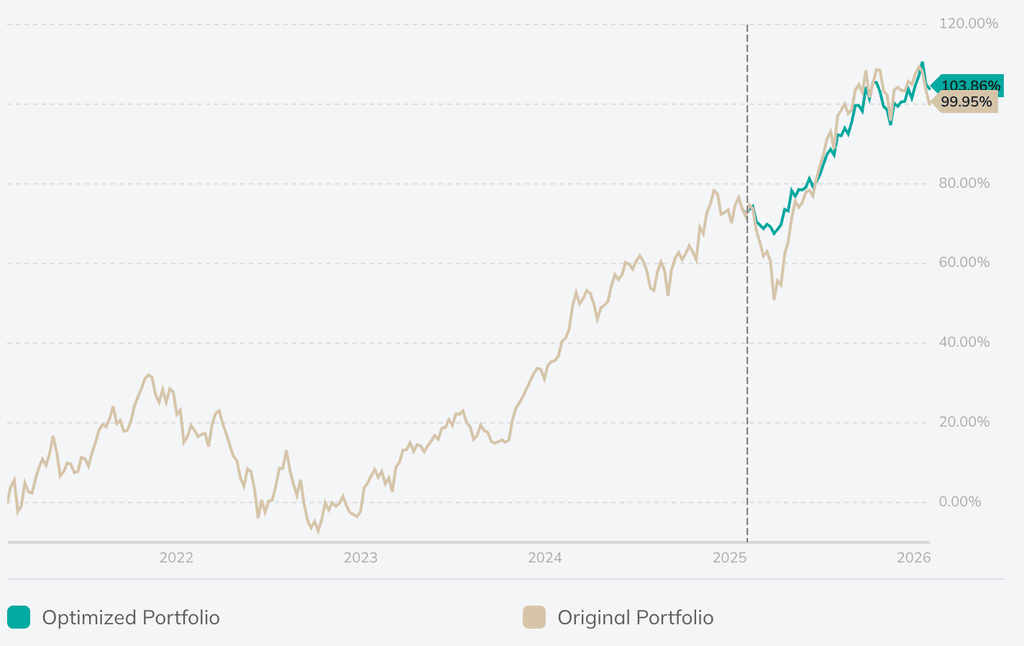

The model was trained on data just before the correction early 2025 (left side of the dotted line) and then selected allocation tested on the real market data throughout 2025 and beyond. HERC results (teal line) show stronger performance with smaller drawdowns on test data compared to equal-weight allocation (beige line).

Try HERC optimization on your portfolio today and see how the algorithm groups your assets into natural clusters.

2 комментария

1 ответ

Сортировать по

Hello Dmitry

I agree with Mr. Berns' comment that HERC optimization tool appears to be useful (converting portfolio holdings to HERC optimization)

One additional suggestion/feedback is that it would be useful if the User could specify the price correlation constant at which clustering occurs. For example, in the benchmark portfolio evaluated HERC defined two clusters; one was associated with precious metals and miners (understandable) and the second cluster is a basket of all other holdings. Some of these holdings have correlations to other components in the second cluster with correlations>0.65. If I manually sort the second basket for holdings with correlations > 0.65 then I would organize the second basket contents into an additional six clusters.

Please advise what your recommended "work around" is for optimizing a HERC portfolio where the second cluster actually has six sub-clusters.

All the best

PS, how will I know when you reply to this comment?

-3 мес.

Hi Dmitry: It appears you have addressed my comments above. I re-ran the portfolio today using the same HERC parameterizations. HERC organized the holdings into 5 clusters. When I manually sort the holding correlation table, the clusters make sense.

Starting the rebalance cycle. Fingers crossed.

Please advise if the above makes sense with HERC program revisions.