Portfolio Optimizer Improvements: Drawdown Minimization and Return Targets

We've added three new capabilities to the Portfolio Optimizer.

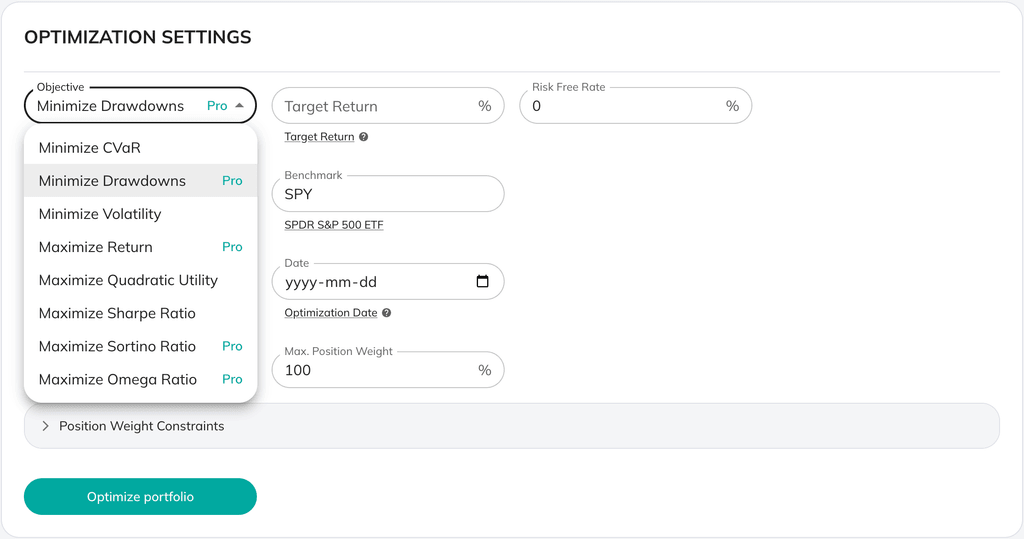

New Optimization Objective: Maximum Drawdown Minimization

You can now optimize specifically to minimize the largest peak-to-trough decline in your portfolio. Unlike variance-based optimization, this directly targets the metric that matters most when capital preservation is critical.

The math is straightforward but the impact is significant: a 40% drawdown requires a 67% gain to break even. For clients nearing retirement or with shorter investment horizons, this objective delivers portfolios designed to weather market downturns without requiring years to recover.

Select "Minimize Drawdowns" from the Objective dropdown when setting up your optimization.

New Constraint: Target Return, %

Set a minimum annual return threshold, and the optimizer will find the lowest-risk portfolio that meets it. By default, the optimizer finds the tangent portfolio, which can be conservative. Setting a higher target return helps you find optimal allocations that minimize risk without sacrificing returns. Note: The target return uses arithmetic mean returns for the optimization model, which may differ from the CAGR displayed in charts and results. This is a standard approach in portfolio optimization theory but worth keeping in mind when interpreting outcomes.

After selecting your optimization objective, you'll see a "Target Return" field where you can enter your desired annual return percentage.

Bonus: Positions Freeze

Now, in the Position Weight Constraints section, you can easily lock individual positions at their current weights while optimizing the rest of the portfolio. Useful for leaving core holdings untouched or for managing tax-sensitive positions. This feature work seamlessly with other existing weight constraints.

0 comments

Sort by